Capturing Long-Term Returns

March 26th 2020 | Categories: Investing |

The following article was shared with us by Zenith Investment Partners, our current Investment research partner. It is technical in nature. If you would like more information or clarification, please reach out to your adviser.

Given the magnitude of market declines caused by the COVID-19 outbreak, investors are undoubtedly focusing on how their portfolios have fared during this period. While often forgotten in strongly rising markets, protecting portfolio capital during a selloff is crucial to achieving better long-term, risk-adjusted returns.

In an ideal world, investors would prefer to minimise their participation in market downturns (known as downside capture) while maximising their exposure during strongly rising markets (known as upside capture). Unfortunately, it isn’t that simple as there is a trade-off between the two. While passive market exposure will have close to 100% upside and downside capture, we believe that investors should aim to build portfolios that balance the two capture ratios to generate superior long-term, risk-adjusted returns. Historically, our portfolios have achieved an upside and downside capture of approximately 85% and 65%, respectively, for balanced risk profiles.

To achieve a better capture balance, portfolios should invest in a range of differentiated strategies to allow elements of the portfolio to perform in both bear and bull markets. Furthermore, by applying active management to a portfolio, any outperformance over passive benchmarks (i.e. active return) can act as an additional diversifier to returns for example during a market selloff, a manager’s positive active return can partially dull the impact of the drawdown.

In this article, we illustrate the benefits of improving the balance between upside and downside capture when compared with a portfolio that fully participates in market rises and falls.

So, what is the upside and downside capture?

Upside capture seeks to measure the level of participation in a benchmark’s positive returns. For example, if a portfolio has an upside capture of 50% and the market generated a return of 10%, we would expect the portfolio to generate a return of 5%.

Conversely, downside capture measures participation in the benchmark’s negative returns. Using the same example, if the portfolio has a downside capture of 50% and the market fell by 10%, the portfolio would be expected to fall by only 5%.

It’s important to note that upside and downside capture ratios are backward-looking and cannot be used to accurately forecast future performance based on market returns. However, these ratios can provide insights as to how sensitive portfolios are in response to market movements and their level of overall diversification.

Comparing an improved capture portfolio to a full participation portfolio

To demonstrate a worked example, we will use a balanced risk profile, with 40% defensive assets and 60% growth assets. We will assume the historical upside and downside capture of approximately 85% and 65%, respectively.

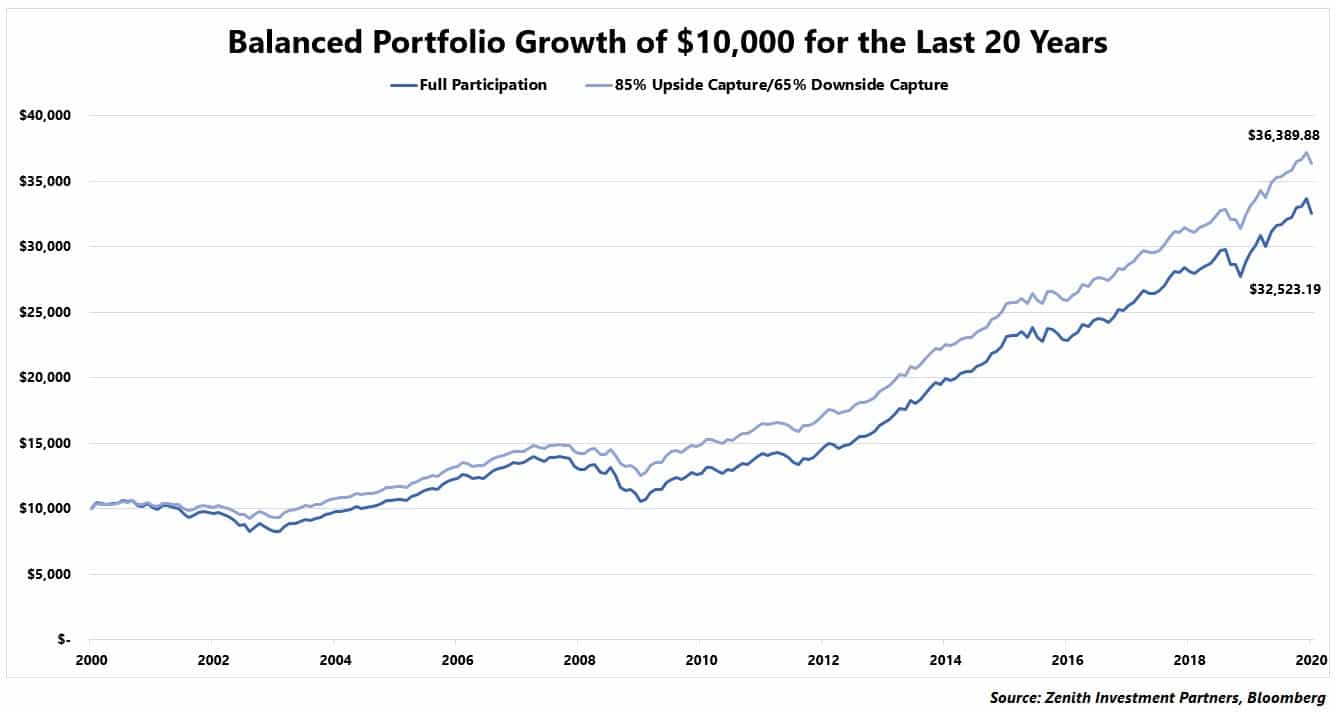

To illustrate the benefits of such an approach, the chart below shows the growth of $10,000 over 20 years ending 29 February 2020 for two balanced portfolios (40% global bonds and 60% global shares). One portfolio has an 85% upside/65% downside capture ratio and the other is a full participation portfolio i.e. 100% upside and downside capture.

As can be seen, the 85%/65% portfolio materially outperforms the full participation portfolio over the 20-year period.

In addition, the 85%/65% portfolio experiences a lower level of volatility than the full participation portfolio as its rises and falls are of a lesser magnitude. As a result, its risk-adjusted returns are also superior to the full participation portfolio as shown in the table below. In essence, investors that achieve these capture ratios are earning a higher level of returns while taking on a lower level of risk when compared with market returns.

| 20 years ending 29/02/2020 | Return (p.a.) | Standard deviation (p.a.) | Return/Risk |

| Full participation | 6.07% | 6.93% | 0.88 |

| 85% upside/65% downside capture | 6.67% | 5.21% | 1.28 |

Source: Zenith Investment Partners, Bloomberg

The Power of Compounding

The secret to these superior outcomes is the better compounding that occurs. By reducing the drawdowns, portfolio balances don’t fall as far as the market during a downturn providing better capital preservation. As a consequence, subsequent returns have a higher capital base to grow from and therefore a higher dollar amount for returns.

The caveat is that when downside capture is improved, investors ultimately are sacrificing some of their upside captures. If the reduction in downside capture is greater than the reduction in upside capture, compounding will allow for superior long-term, risk-adjusted return outcomes.

Conclusion

During these uncertain markets, it’s understandable that investors are focused on preserving capital. However, by constructing a well-diversified portfolio from the outset, the trade-off between downside capture and upside capture can be improved to benefit from greater compounding of returns over the longer term.

Important Notes

The benchmark used for the growth of $10,000 comprises the following:

- 30% MSCI World ex Australia (AUD Hedged)

- 30% MSCI World $A Unhedged

- 40% Bloomberg Barclays Global Aggregate Index (AUD Hedged)

Where the benchmark generates a positive monthly return, the 85% upside/65% downside capture portfolio will have a monthly return of 85% of the benchmark’s return. Where the benchmark generates a negative monthly return, the portfolio will have a monthly return of 65% of the benchmark’s return.

Reach out to us today for more information.

[ninja_form id=41]

Source: Zenith Insights

Posted in Investing