Good debt, bad debt, debt recycling

March 20th 2016 | Categories: Debt Management |

For some people, the notion of ‘good’ debt is inconceivable. But by including debt recycling in your investment strategy, you could discover new possibilities for your financial future. The word ‘debt’ can invoke a range of reactions. For some, it is terrifying and to be avoided. For others, it is a means to an exciting end. For most, it is simply inevitable, and will at times be a source of joy, stress, fear, and everything in between.

The good and the bad

‘Good debt’ is the kind of debt we undertake when we buy something that is likely to increase in value (such as a well researched investment). It is supported by an adequate income stream, and/or will go on to generate its own income. ‘Bad debt’ is the kind of debt that burdens us. It is for things that decrease in value and do not produce their own income, such as a boat, credit card debt, and so on. When we have good debts and reliable income coming in beyond repayment obligations, there are opportunities to leverage our debt to grow our investments. One example of this kind of strategy is a principle called ‘debt recycling’.

Debt recycling

Debt recycling allows you to invest for the future while continuing to pay off your home loan. Basically, your property and assets are used as security to borrow funds to service an investment loan. The income generated from the investment and any tax advantages are used to pay off non-deductible debt on your home loan. The investment loan is then increased by the amount you have paid off the mortgage or non-deductible loan, and the money is reinvested. This process is repeated until eventually the non-deductible loan is replaced by the deductible loan. In other words, debt recycling is the process of creating an ongoing cycle that turns ‘bad’ debt into ‘good’ debt, so you can pay off your home loan sooner.

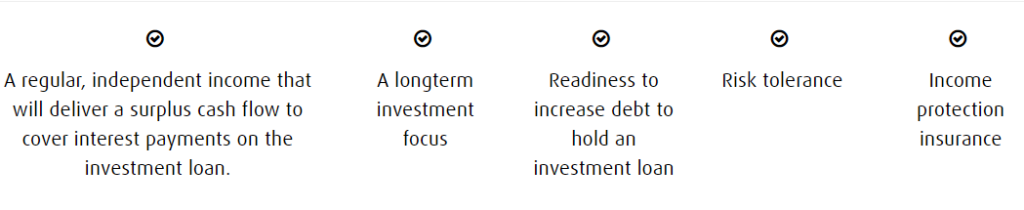

For this type of strategy to work, there are a number of things you need:

Overtime, the non-deductible debt from the original mortgage is converted into deductible debt, which could have the potential to save you thousands on interest expenses.

Contact us

Like many other financial strategies, debt recycling involves risk. It is best to work with a Financial Planner to develop a strategy that will work for you.

Want a Complimentary Consultation?

Fill in the form for a complimentary consultation with a Financial Adviser and start living your best possible life.

What you need to knowThis information is provided by Invest Blue Pty Ltd. (ABN 91 100 874 744). The information contained in this article is of general nature only and does not take into account the objectives, financial situation or needs of any particular person. Therefore, before making any decision, you should consider the appropriateness of the advice regarding those matters and seek personal financial, tax and/or legal advice before acting on this information. Read our Financial Services Guide for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you.

Posted in Debt Management