Guide for guarantors

September 6th 2022 | Categories: Home Loans & Leveraging Equity |

The ultimate guide to becoming a guarantor

What does it mean to become a guarantor?

A guarantor is someone who agrees to be responsible for repaying a debt owed to a lender for a loan provided to another individual or business if the borrower can’t make their repayments.

A guarantor supports the loan by providing lenders with additional security such as a property they own. By providing a guarantee, lenders may lend to the borrower in situations where they may not have been able to secure the full amount on their own.

This guide outlines the important information and risks to consider before becoming a guarantor.

What are the risks if you choose to provide a guarantee?

This is an important decision to make and therefore you should consider it carefully.

If you choose to provide a guarantee, you’ll be signing a legal contract in which you agree to repay the home loan if the borrower can’t meet the repayment terms and conditions of their loan contract. If the borrower is unable to repay their home loan, lenders will first seek to recover the debt from the borrower (by stepping in to assist with the sale of the borrowers’ security), before they seek any security you have provided in support of your guarantee (unless they reasonably expect that after doing so, a substantial amount would still be owing).

The amount shown in the guarantee could be the entire amount of the borrower’s loan or a limited amount, and you may be required to pay lenders the maximum amount shown in the guarantee, along with interest and reasonable enforcement expenses. If lenders lend more money to the borrower at a later stage, either under the original loan contract or a new one, your guarantee will cover the additional borrowing too.

There are a number of important points to consider when you choose to become a guarantor. Here are some of the ways your financial situation may be impacted.

When security support (only) is provided, some lenders will assess the home loan application based on the borrowers’ financial information, others will require you to prove that you can afford to repay the guaranteed loan amount yourself. Some lenders allow you to limit the amount you are liable for under the guarantee. Lenders can say no to your request if:

• The limit you propose is less than what the borrower owes to them;

• Lenders are obliged to make further advances or enter into further arrangements with the borrower; or

• Lenders would be unable to secure the present value of an asset which is security for the loan (such as a house under construction). You can withdraw from the guarantee through a written request.

• Before lenders provide any money to the borrower(s) under the loan contract; or

• After any money is first provided if the final loan contract is materially different from the one the lender gave you before your signed the guarantee.

You can be released from the guarantee when your guarantee is no longer required by the lender. This could occur when the guaranteed amount is paid off by the borrower(s) and the loan is reduced. Alternatively, you can end your financial obligation under the guarantee at any time by:

• Paying the lender any money the borrower(s) owes at the time, including any further amounts they’re obliged to provide the borrower that are covered by your guarantee;

• Paying the lender the maximum amount you’re required to under the guarantee; or

• Suggesting another arrangement that the lender agrees to.

Explore our Knowledge Centre below for more insights.

Meet Tom & Andrew

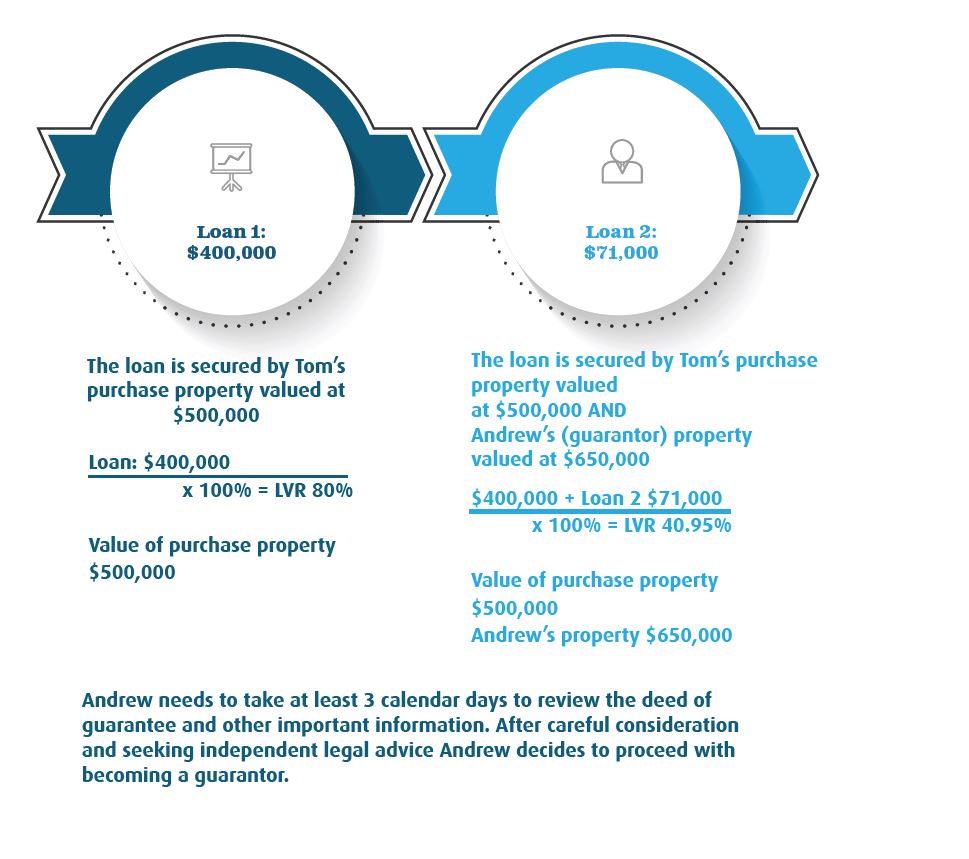

Tom wants to purchase his new home with additional security from Andrew, his father. He doesn’t have enough genuine savings to enable a 20% deposit, however, can service the loan amount required. Andrew has offered to provide a guarantee over his unencumbered property to enable Tom to purchase the home without the need to pay Lenders Mortgage Insurance (which may be required if his Loan to Value Ratio (LVR) is greater than 80%). Let’s have a look to see how the loan is structured and what happens next.

How does it work?

Tom is purchasing a home for $500,000. He has saved a total of $71,000 ($50,000 for their deposit and $21,000 for their additional costs such as stamp duty and legal fees). Tom is looking to borrow a total of $471,000 Their Invest Blue Mortgage broker speaks to Andrew alone to explain the obligations and risks associated with becoming a guarantor. After careful consideration, Andrew proceeds with providing a guarantee. To limit Andrew’s guarantee liability, Tom will split his loan as follows:

Next steps, after choosing to become a guarantor

Before lenders will accept a guarantee from you, there are a few key steps to follow. We will ask you to sign and return some preliminary forms to verify your identity and agree to the lender’s specific privacy policy. Lenders will give you information about the borrower(s) financial situation and the loan they’re applying for, along with a deed of guarantee and a guarantor acknowledgement form for you to sign.

This information may include:

• The proposed loan contract and a list of any related security contracts;

• Any related credit report from a credit reporting body;

• Any financial accounts or statements of the financial situation the borrower has given them in the previous two years for the purpose of the guaranteed loan;

• The latest statement of account relating to the loan for a period in which a notice of demand was made by them within the

• Any notice of demand they have made on the borrower for the guaranteed loan, or any loan the borrower has (or has had) with them, within the previous two years;

• If any existing loan they have given the borrower will be cancelled if the guarantee is not provided; and Any current credit-related issuance contract that is in their possession

Lenders will ask that you take at least three calendar days to review all this information and carefully consider if you want to provide a guarantee. If you choose to provide a guarantee, they will ask you to:

• Sign the deed of guarantee before an eligible witness (as outlined in the guarantee documentation), without the borrower(s) being present; and

• Confirm on an acknowledgement form that you’ve taken at least three calendar days to review the information before signing.

Note: Lenders can accept the guarantee earlier if you have obtained independent legal advice about it.

Remember it’s okay if at any stage you choose not to proceed with providing a guarantee.

Important: If you’re becoming a guarantor as the sole director of a company borrower, or you’re a trustee guarantor, you may choose not to receive some or all of the documents, however, they contain important information that may affect your decision to give a guarantee. Also, the three calendar day review period requirement won’t apply to you.

Some FAQS

How is a co-borrower different to a guarantor?

• A co-borrower is someone who chooses to borrow money with another individual or business. A co-borrower is responsible for regular repayments on their home loan and repaying the loan in the event of a default.

• A guarantor will only become liable for the amount they have guaranteed (which could be up to the full amount of the home loan, along with interest and reasonable enforcement expenses) in the event the borrower(s) can’t meet the repayment terms and conditions oftheir loan contract.

What information can I ask for during the life of the loan?

• You can ask the lender at any time for a statement of the amount the borrower(s) currently owes, any amounts debited or credited, overdue amounts and when they became overdue. This information may be given to you verbally unless you ask for it in writing.

• The majority of lenders will also give you the following information about a borrower’s deteriorating financial situation as it relates to the loan you guarantee, within 14 days of the relevant event:

– A copy of any formal demand or default notice sent to the borrower;

– A written notice if the borrower has advised that they are experiencing financial difficulty which has resulted in a change to their loan; and

– A written notice if the borrower is in continuing default for more than two months after the issuance of the default notice referred to above. This does not apply if you’re a sole director guarantor or trustee guarantor.

Will becoming a guarantor affect my future borrowing capacity?

• When you apply for credit, you may need to tell the credit provider about any loans you are a guarantor on. This may affect your borrowing capacity, especially if you want to borrow against the property you have provided as security

Book a chat with us if you would like to speak with one of our other financial advisers.

Want a Complimentary Consultation?

Fill in the form for a complimentary consultation with a Financial Adviser and start living your best possible life.

What you need to know: This information is provided by Invest Blue Pty Ltd (ABN 91 100 874 744). The information contained in this article is of general nature only and does not take into account the objectives, financial situation or needs of any particular person. Therefore, before making any decision, you should consider the appropriateness of the advice with regards to those matters and seek personal financial, tax and/or legal advice prior to acting on this information. Read our Financial Services Guide for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you.

Posted in Home Loans & Leveraging Equity