New financial year, new super changes

July 9th 2021 | Categories: Superannuation & SMSF |

Some, like the rise in the Superannuation Guarantee (SG), will happen automatically so you won’t need to lift a finger. Others, like higher contribution caps, may require some planning to get the full benefit.

Whether you are just starting your super journey or close to retirement, a member of a big super fund or your own self-managed super fund (SMSF), it pays to know what’s on offer.

Here’s a summary of the changes starting from 1 July 2021.

Increase in the Super Guarantee

If you are an employee, the amount your employer contributes to your super fund has just increased to 10 per cent of your pre-tax ordinary time earnings, up from 9.5 per cent. For higher income earners, employers are not required to pay the SG on amounts you earn above $58,920 per quarter (up from $57,090 in 2020-21).

Say you earn $100,000 a year before tax. In the 2021-22 financial year your employer is required to contribute $10,000 into your super account, up from $9,500 last financial year. For younger members especially, that could add up to a substantial increase in your retirement savings once time and compound earnings weave their magic.

The SG rate is scheduled to rise again to 10.5 per cent on 1 July 2022 and gradually increase until it reaches 12% on 1 July 2025.

Chat to our team to see how you can make the most of these benefits

[ninja_form id=37]

Higher contributions caps

The annual limits on the amount you can contribute to super have also been lifted, for the first time in four years.

The concessional (before tax) contributions cap has increased from $25,000 a year to $27,500. These contributions include SG payments from your employer as well as any salary sacrifice arrangements you have in place and personal contributions you claim a tax deduction for.

At the same time, the cap on non-concessional (after-tax) contributions has gone up from $100,000 to $110,000. This means the amount you can contribute under a bring-forward arrangement has also increased, provided you are eligible.

Under the bring-forward rule, you can put up to three years’ non-concessional contributions into your super in a single financial year. So this year, if eligible, you could potentially contribute up to $330,000 this way (3 x $110,000), up from $300,000 previously. This is a useful strategy if you receive a windfall and want to use some of it to boost your retirement savings.

Major changes are also coming to insurance protection. You can read more about that here.

More generous Total Super Balance and Transfer Balance Cap

Super remains the most tax-efficient savings vehicle on the land, but there are limits to how much you can squirrel away in super for your retirement. These limits, however, have just become a little more generous.

The Total Super Balance (TSB) threshold which determines whether you can make non-concessional (after-tax) contributions in a financial year is assessed on 30 June of the previous financial year. The TSB at which no non-concessional contributions can be made this financial year will increase to $1.7 million from $1.6 million.

Just to confuse matters, the same limit applies to the amount you can transfer from your accumulation account into a retirement phase super pension. This is known as the Transfer Balance Cap (TBC), and it has also just increased to $1.7 million from $1.6 million.

If you retired and started a super pension before July 1 this year, your TBC may be less than $1.7 million and you may not be able to take full advantage of the increased TBC. The rules are complex, so get in touch if you would like to discuss your situation.

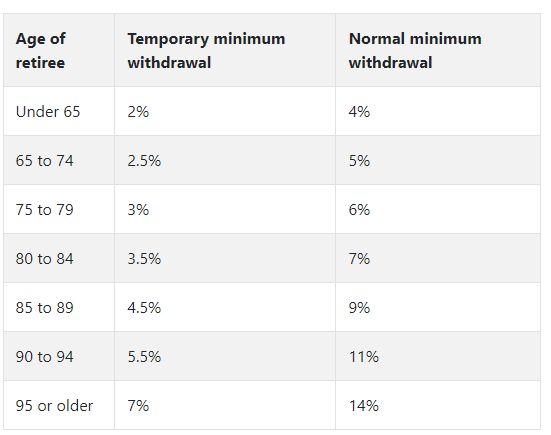

Reduction in minimum pension drawdowns extended

In response to record low-interest rates and volatile investment markets, the government has extended the temporary 50 per cent reduction in minimum pension drawdowns until 30 June 2022.

Retirees with certain super pensions and annuities are required to withdraw a minimum percentage of their account balance each year. Due to the impact of the pandemic on retiree finances, the minimum withdrawal amounts were also halved for the 2019-20 and 2020-21 financial years.

You can read more about this here.

But wait, there’s more

The next financial year is also shaping up as a big one for super, with most of the changes announced in the May Federal Budget expected to start on 1 July 2022.

The Budget included proposals to:

- repeal the work test for people aged 67 to 74 who want to contribute to super

- reduce the minimum age for making a downsizer contribution (using sale proceeds from your family home) from 65 to 60

- abolish the $450 per month income limit for receiving the Super Guarantee

- expand the First Home Super Saver Scheme

- provide a two-year window to commute legacy income streams

- allow lump-sum withdrawals from the Pension Loans Scheme

- relax SMSF residency requirements.

All these measures still need to be passed by parliament and legislated.

You may be interested in reading up on:

- how much super do you need for a comfortable retirement

- divorce and superannuation – how is it split

- is salary sacrificing worth it

Time to prepare

There’s a lot for super fund members to digest. SMSF trustees in particular will need to ensure they document changes that affect any of the members in their fund. But these latest changes also present retirement planning opportunities.

Whatever your situation, if you would like to discuss how to make the most of the new rules, please get in touch.

[ninja_form id=41]

What you need to know

This information is provided by Invest Blue Pty Ltd (ABN 91 100 874 744). The information contained in this article is of general nature only and does not take into account the objectives, financial situation or needs of any particular person. Therefore, before making any decision, you should consider the appropriateness of the advice with regards to those matters and seek personal financial, tax and/or legal advice prior to acting on this information. Read our Financial Services Guide for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relations to products and services provided to you.

Posted in Superannuation & SMSF