Your super & covid-19

October 15th 2020 | Categories: Financial Planning |

Throughout the Coronavirus pandemic we have been able to help our clients navigate any changes they face to their financial position, throughout this time we have also received a number of queries in regards to changes to superannuation, the 10k super early release and how to get your super balance back on track. To help answer your questions we are joined by Tony Martin. Tony is Financial Planner with Invest Blue located in Rockhampton and specialises in strategic advice, retirement planning and financial improvement strategies.

Q. How concerned should we be about current super performances?

Superannuation by design is a long-term investment, with strict rules on accessibility. Accumulators that are still working and have timeframe until retirement should not be overly concerned, as their employers are paying 9.5% Superannuation Guarantee Contributions into their nominated super accounts on a regular basis, which will assist navigating through shorter-term volatility and will ensure that longer-term gains are still achieved. Even those that are about to enter retirement or perhaps in retirement should not be overly concerned either, as retirement timeframes are still long term. Financial advisers can provide clarity and understanding of your risk profile, capital value and abilities to generate a certain income that will give you the necessary understanding to make informed lifestyle decisions throughout retirement.

Markets move up and down, that is normal. A good investment strategy will factor in significant downturns as well. While we can predict when they will happen, we do know that they do occur and recommend that people are prepared for that. This largely points to the balance between risk and return. If your investment strategy takes both of those elements into consideration, and they also reflect you and your goals, then you are well-positioned to ride out the storm. If you are unsure, now is the best time to get an expert opinion.

Q. Should I be investing inside or outside of my super?

Deciding whether you to invest inside or outside of your super will be different for each person based on your personal dreams and goals. As I mentioned above superannuation is a long-term investment and generally, you won’t be able to access it until you reach your retirement age. Given this, your life stage will also need to be taken into consideration when making this decision.

There are tax benefits that come with investing in super and management of your investments is also looked after by your super fund provider which can reduce fees and also account management time, however, there is less flexibility in terms of accessibility and superannuation is subject to change as it regulated by the government.

It’s also worth mentioning superannuation is invested in a diversified portfolio of assets including shares, bonds, cash and listed property. Therefore, you may achieve the same results by investing outside of your super. It all comes down to having a clear picture of what your goals are and from there we can work together to choose the right investment choice for you.

You may find the below articles useful:

- Buying shares v’s investing more in your super

- A guide to choosing the right investment

- Is now a good time to invest in shares

Q. I withdrew 10K from my super, how can I replenish these funds?

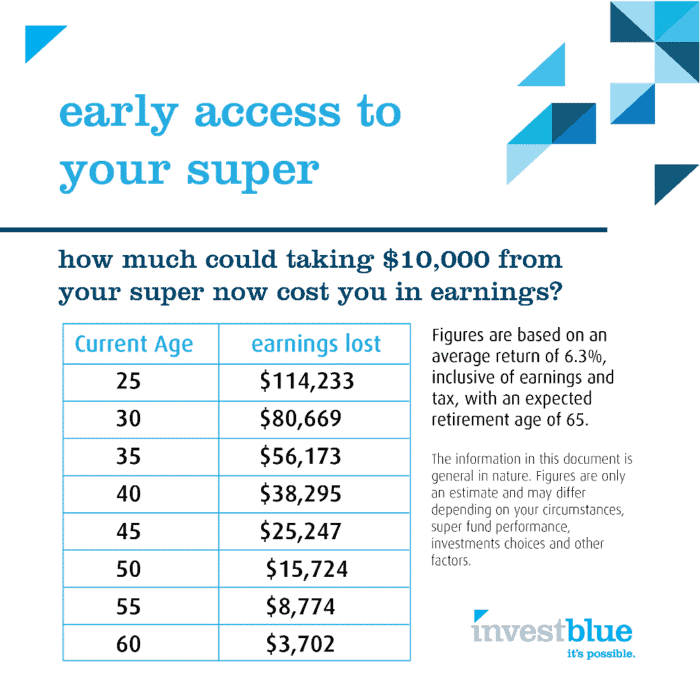

There are various ways you could get your retirement funds back on track if you withdrew from your super during the pandemic. We can see in recent reports that 40% of Australians who accessed their super had no decrease in household income and 64% of their withdrawal went to non-essential items which is a cause for concern. Depending on your age, an investment of $10k in your super could grow by as much as $114,000 in compounding interest by the time you hit retirement which is why implementing a strategy to replenish these funds is important.

Strategies to top up super:

- Make additional contributions, perhaps from bonuses, tax returns or lump sum payments

- Put a bit away each fortnight through salary sacrifice (hint – this can help you save on tax as well)

- If you’re approaching retirement you may consider downsizing your property to reduce debt and boost your super through a lump sum contribution with the net proceeds

- Review your super funds’ fees and portfolio performance

You can read more about this in our article boosting your supper after a 10k withdrawal

Q. Should I access the 10k to use towards my home loan or house deposit?

Firstly, your super is an important asset and should and be treated the same way you would treat any other investment. In comparison, if you could withdraw $10k from your home equity, would you? Before accessing the early release of the super scheme this is something to keep in mind especially considering your super is an asset that is most likely going to grow in value over time (on average 6.3% per annum, as shown in the table above).

Secondly, if you do choose to access your super you should carefully consider where you are spending it, given 64% of spending is going towards nonessentials. With that said the only real way to gain value from withdrawing your super is to reinvest it in another asset that could grow in value such as property or shares outside of your super. Under the early release of the super scheme, withdrawals are tax-free and therefore it could present an opportunity to get your foot in the door of your next investment where otherwise you may not be able to do so.

Q. Are there any other pros or cons to withdrawing from super under the Covid-19 allowance?

Keep in mind if you withdraw from your super, some lenders won’t lend to you for up to three months as it appears on your credit report as financial hardship.

It’s also worth mentioning this scheme was designed for people financially impacted by Covid-19 and should be utilised if you need to use it.

If you are financially impacted due to the Coronavirus you may find our COVID-19 support page useful.

Once again, before making any financial decisions your dreams and goals, life stage and budget should all be taken into consideration. Before acting on any decision around your super it is always worth having a financial planner review your options and ensure they are aligned to your unique situation and needs.

Tony Martin

Financial Adviser

Connect with Tony on LinkedIn

Next month we are joined by one of our Melbourne Financial advisers, discussing how to live your best possible life in retirement and strategies to help get you there. If you have any questions you want to be answered about your retirement, drop them in the form below and they may be featured in next month’s issue of Ask an Adviser.

[ninja_form id=66]

What you need to know

This information is provided by Invest Blue Pty Ltd (ABN 91 100 874 744). The information contained in this article is of general nature only and does not take into account the objectives, financial situation or needs of any particular person. Therefore, before making any decision, you should consider the appropriateness of the advice with regards to those matters and seek personal financial, tax and/or legal advice prior to acting on this information. Read our Financial Services Guide for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relations to products and services provided to you.

Posted in Financial Planning