Why is my fund under-performing?

November 8th 2019 | Categories: Superannuation & SMSF |

When we carve out hard-earned dollars and squirrel them away in an investment, whether it be in Super or not, it can be worrying if we think our choice is not performing well against others. No one wants to think they made a mistake in their investment selection. It’s natural to want to make the most of what we have. So how do you compare your investment to others? Is your investment underperforming? How do you know?

Understand how a financial adviser can support you with your need for financial security. Get in touch.

[ninja_form id=37]

Defining performance

When we think about investment performance, we are usually considering what the return has been over a specific time frame. You might see that a fund has returned 5% over 12 months. Is that good?

Performance is only a concept that can be understood when it is put into context, and this is where we often see people struggle. Sure you can look at Fund A and Fund B and see that one has done 1% better over the last year, but what does that mean really?

When considering a return, you also need to consider the following elements:

- What were you expecting the return to be?

- How long a timeframe are you reviewing?

- What risk was taken to earn that return?

- What costs are associated with belonging to that fund?

- What other benefits does the fund provide?

When you get a clearer picture of your context, performance starts to make a bit more sense.

Managing Expectations

As financial advisers, we will work with you to understand what is most important to you – clarify your dreams and goals and prioritise them. In doing this we paint a picture of what your best life looks like. We then get a clear understanding of your current situation, your financial life and how you feel about choices around risk. This then lets us model your best possible life in a very visual way. To do this we build a plan based on a set of assumptions. Those assumptions will include a rate of return in line with your comfort of risk and goals. It is these expectations we keep an eye on.

If a fund is performing better than expected, it can add to your wealth and improve the forecast; but we also keep in mind that the time horizon will play an impact on the overall outcome. All funds have good years and bad as the markets move more broadly. What we want to see is that the fund performs to the average expectation over the medium to long term. If it isn’t, then it is time to change.

What is the right time frame to consider?

If you are determining a fund’s performance, should you compare the last 12 months, 5 years, 10 years? By in large, the longer timeframe gives you a clearer picture as this demonstrates consistency and evens out the inevitable yearly variability. Be aware of the disclaimer though, past performance is not a guarantee of future returns.

It also comes down to where you are at in your own life. What is your investment horizon? Generally speaking, the younger you are the longer your investment timeframes.

“If a balanced fund has done 7% over the year, it has done better than expected – you need to be prepared that there is likely a time of worst performance coming,” says Tom Merrick, Financial Adviser Coffs Harbour. “You have to take the timeframe and market conditions into account when looking at how well an investment is doing.”

Is the reward worth the risk?

Risk is often the part of the equation that gets forgotten, particularly in bullish years when markets are doing well. The basic principles in investing are that the higher return you are chasing, the more likely it is that you will have to take on more risk. So, in a higher risk ‘growth’ type investment, when the going is good, your returns will be higher, but when markets go down, the likelihood of losses or much weaker performance is also higher.

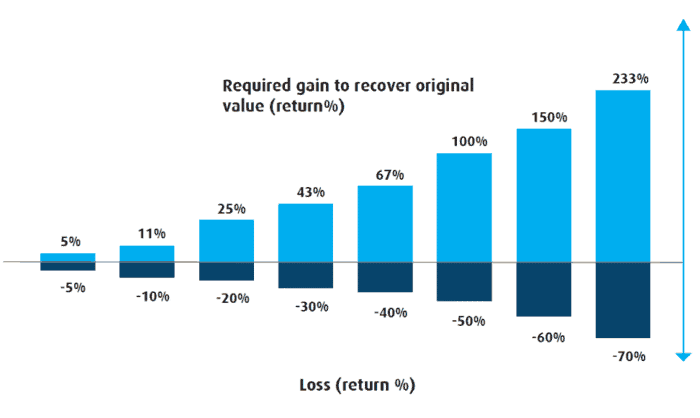

Our investment philosophy is that both risk and reward must be considered when building an investment strategy for a client. Earning your desired return is as important as protecting you from losses. If you lose a dollar today, it will take an increasingly larger amount of investment and positive return to recover from that.

So, Fund A may be ‘outperforming’ Fund B today, but have they taken the same risk profile? What is likely to happen with each fund in a downturn? What will the performance be over the long term? These are all factors that need considering. Funds usually describe their risk profile on a scale between conservative, balanced and growth; but the actual make-up of these funds may vary widely. What is ‘balanced’ for one fund, may actually be considered as ‘growth’ in another. So how do you pick the right one for you? Having a good read of the makeup of the funds and the managers approaches is important.

“We have had a bull market in recent years. If your portfolio is heavily weighted towards index and growth style funds, it will have done well since the Global Financial Crisis of 2007/8. However, when there is a downturn, there will be more potential for volatility and risk of experiencing losses.”

Tom Merrick adds that “Part of making money is not losing money. The advertised performance of one fund to another needs to be considered more fully before you can determine the suitability for a client. Perhaps the fund you have now is relatively conservative to be in line with an appropriate level of risk for your situation and your goals. Comparing what you have to another ‘growth’ fund isn’t comparing like for like. If more growth is what you are after, then we need to have a deeper conversation about your values and goals and appetite for risk. Our job is to align investment selection with the whole financial picture for a client.”

To fee or not to fee, that is the question

Not all funds are created equally when it comes to fees. In fact, there can be quite a variation in the costs associated with buying into, holding or selling an investment. Comparing one set of fees to another can also be a challenge, as there are a number of fee types and not all funds list their fees in the same way. What fees are likely involved?

- Management fees: these typically range from 0.19-1.00% of managed funds[1]

- Administration fees: these can range from 0-0.15%

- Investor/low balance fee: these are rare but do exist for some funds if the holdings drop below a certain level

- Performance fee: not all funds have these and the cost for those that do can vary widely

- Transaction Fee: this happens when you contribute to or withdraw from your fund and can range from 0-1%

- Account fees: some funds charge for things like opening or closing the fund, contributions or redemptions.

Performance needs to take into account the costs and benefits provided in addition to the return on investment.

Benefits

Super funds often come with an insurance package, and if you have held your fund for a long period of time, that insurance package may be valuable to you. Replacing that policy years later as you have aged and potentially experienced health conditions could be quite expensive. One fund’s coverage and claims experience may also vary from another’s.

This is a good place to point out that there are a staggering number of cases we have worked with where a person had had an illness or injury that was claimable under their insurance policy, but they had not made a claim. If you have had an accident or illness, it can be worth speaking with an adviser to see if there are grounds to make an insurance claim.

When you are comparing the performance of one super fund with your existing fund, the benefits you hold inside your fund need to also be considered.

What role do we play in our investment’s performance?

Human nature can work against us when it comes to managing our own investments. Successful investor Warren Buffet is often quoted saying “Be fearful when others are greedy and greedy when others are fearful”. This is counterintuitive to the way many moves with the market. When it is crashing, it is easy to be scared of what is happening to your investment. You see the value dropping and you want to put a stop to it. This is when a sale can hurt – getting out when markets are low means you have realised the loss, and as described earlier in this article, it will take a lot to regain that loss.

Similarly, when the going is good and we see others doing well in a rising market, confidence can be at a high. We are tempted to jump in. Carl Richards, an expert in Behaviour Finance talks about the behaviour gap. This gap describes the difference between what we want for our financial lives and what we actually do. Psychology or human behaviour is what lives in the middle. So how do you avoid the pitfalls of psychology and money?

If we are the ones responsible for moving money in and out of investments, it can be very difficult to remove our own emotion. That can impact your overall investment performance. Working with someone else who can take an experienced, objective stance on the decisions around your investments is a great way to reduce personal bias and risk.

How important is performance vs. what we do with our money?

No amount of return will save a leaking ship – if you are spending on things that don’t really matter to you, that doesn’t add to your quality of life in a way that is meaningful to you, that doesn’t contribute to your most important dreams and goals – the cost of that can erode gains and leave you feeling dissatisfied.

The manner in which you contribute to your investments also has an impact. If you put an amount in consistently over a long timeframe, you will take advantage of ‘dollar cost averaging’. The power inherent in this approach is that you will be buying in at all stages of the market cycles – sometimes the market will be down and you will get more for your investment. Sometimes it will be high and you will be paying top dollar. Contributing consistently means that you don’t have to worry about timing the market, you just participate regularly, taking the good with the bad and letting the power of compound interest do its thing, growing your portfolio, on top of a growing investment base, over time.

Does performance matter?

If you set out a plan, identify your goals and you can afford them, what impact would that extra percentage point make?

There will always be moments in time when, with hindsight, you can find a fund or investment that has done better than the one you are in. How do you manage that? Should you? We believe that it is important to monitor the quality of the fund and the decisions it is making, but not necessarily ensuring that it is the top performer for every time frame you can consider, at any moment in time. If the fund is meeting its targets over time, then it is doing the job we need it to do.

It is important to consider the impact performance has had on your current situation and future. When you continue to look forward, we can model out your current situation and what your future is likely to look like and ask the important questions: will you be able to realise your important dreams and goals? Will you have the lifestyle you are hoping for? That is the measure we consider most important. And your investment’s performance? Well, it just needs to come close to the assumptions made when selecting it.

Things are just not adding up, now what?

Having read all of this, you may still be wondering “when should I consider changing my investment”? We can’t tell you that specifically because every person has a different set of circumstances, goals, objectives, tolerance for risk, etc…, but there are some things to consider:

- Are all your eggs in one basket? If you are heavily invested in one area, that lack of diversification can expose you to more risk than you have bargained for.

- Does the risk profile of your investment match your appetite? Every investment comes with its own inherent exposure to risk and it isn’t always easy to determine what that is. One fund’s “balanced” portfolio is another’s “growth”, stay in tune with that. Learn more about choosing the right fund here.

- Are you paying appropriate fees for holding and working with the investment? Every investment comes with fees. Fees to join, manage, change, leave. There can be wide differences from one to another and it is worth investigation.

- Has your investment profile kept pace with changes in your life? As you move through the cycle of life, your needs, attitude toward risk and investment horizon all change. Your investment profile needs to move with you. Do you know what you need right now? Do you understand how your investment mix fits?

- Who is looking after the day to day management? Understanding what is happening in the market and adapting your portfolio to ensure it remains within your risk profile can be a big job. If this is something you are doing yourself, you need to ensure your lifestyle allows for the time to do research and make decisions. We also recommend engaging a third party to help to dilute the emotional impact investing your own money can have on your decision making. At Invest Blue we work with a third party to manage the investment platforms for our clients. Our Investment Philosophy advocates for professional, external, specialist research firms to be involved in asset selection and ongoing management. “With the platforms we recommend, the benefit of the active managers we have is that they can make decisions about what the market is likely to do. For example, if they think the market is at a high, they may hold more cash for stability in a downturn. There is an opportunity to mitigate risk on an ongoing basis.” Explains Tom Merrick.

- What will it cost to change? There may be exit costs to consider.

Try our investment report card to see where your current portfolio sits.

[1] https://www.canstar.com.au/managed-funds/managed-funds-how-do-fees-compare/

Financial Advice is only a phone call away. Set yourself on a path to financial freedom. Contact us or ask us a question today.

[ninja_form id=41]

What you need to know

This information is provided by Invest Blue Pty Ltd (ABN 91 100 874 744). The information contained in this article is of general nature only and does not take into account the objectives, financial situation or needs of any particular person. Therefore, before making any decision, you should consider the appropriateness of the advice with regards to those matters and seek personal financial, tax and/or legal advice prior to acting on this information. Read our Financial Services Guide for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relations to products and services provided to you.

Posted in Superannuation & SMSF